A review of the Australian payments system has recommended a stronger role for the federal government, through the Treasurer, in setting the strategic direction of the system. This includes enabling the treasurer to ”direct regulators to develop regulatory rules” and ”give binding directions to operators of, or participants in, payments systems”.

The recommendations were just a few of the 15 changes to the payments system called for in a review [PDF] probing Australia’s 20-plus year-old regulatory architecture for payments.

The Payments System Review also called for further consideration to be given to how digital wallets, buy-now, pay-later (BNPL), central bank digital currencies, cryptocurrency, and de-banking interact with the new regulatory architecture.

As such, one recommendation was for the creation of defined list of payment functions that require regulation.

“This should be used consistently across all payments regulation,” the review states. “The list should be able to change to ensure it remains fit-for-purpose as technological advancements gather pace.”

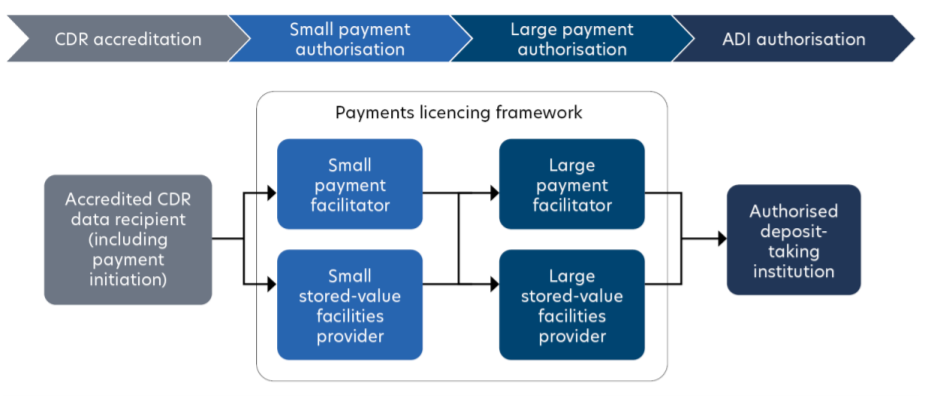

It also called for the introduction of a single, tiered payments licencing framework.

Proposed single licencing framework

A single payments licencing framework should boast separate authorisations for the provision of payments facilitation services and the provision of stored-value facilities, and two tiers of authorisations based on the scale of the activity performed by the payment service provider, the review states.

The solution proposed is one licence that is scalable based on the payment function sought to be provided. This would mean a small new entrant would not face the same regulatory obligations as a larger, more established one performing a wider range of activities with a higher volume of payments.

See also: Sweeping change: Fintech committee offers ‘quick wins’ fix to Australian ecosystem

The review said that given the number of regulators with responsibilities in the space — Reserve Bank of Australia (RBA), Australian Securities and Information Commission, Australian Prudential Regulation Authority, Austrac, and the Australian Competition and Consumer Commission — there is a need for a consistent policy approach.

Additionally, it recommended the regulators strengthen their coordination and adopt a more functional approach. This requires a regulator to look at the nature of the service, not the entity that is providing it, given the expansion of digital wallets such as Apple Pay and Google Pay.

“Today’s regulatory architecture was designed to accommodate the technology, providers and business models of the payments system more than two decades ago,” it says.

“While the reasons for regulation — to ensure the safety, efficiency, and effectiveness of payments — have not changed over time, the sources of risks have evolved, necessitating the need for regulation to respond.”

The review said the safety, efficiency, and effectiveness of payments can now be affected by providers that are not within the traditional payments industry, and that the disintermediation of the payments process by fintechs has changed competitive dynamics.

“It has led to more layers of competition and new issues relating to access to payment systems. The diverse range of new [payment service providers] is also making system-wide cooperation more difficult. The shift in the source of risks within the payments ecosystem warrant a change in the regulatory approach to ensure payments remain safe, efficient, and effective for consumers and businesses,” it says.

The review said the ePayments Code should be mandated for all holders of the payments licence, and, accordingly, the ePayments Code should be brought into regulation.

“The common access requirements for payment systems should form part of the payments licence to facilitate access for licensees to those systems,” it said, noting the RBA should develop common access requirements in consultation with the operators of payment systems.

Toying with the idea of giving further regulatory power to existing finance-related bodies, the review concluded the government, through the Treasurer, is best placed to provide enhanced leadership, vision, and oversight.

The Treasury’s enhanced function, the review said, should not replace or duplicate the roles of the RBA or other financial regulators. Rather, it should complement the work of the regulators by articulating the government’s stance on payments issues, involve relevant stakeholders to identify trends in the market, and provide the platform for regulators to work together to address key payments issues.

The Treasurer should be the one appointing a payments industry convenor to collaborate with regulators and industry to develop the strategic plan, identify issues, coordinate responses, and provide strategic advice to the Treasurer on payments-related matters.

The payments industry convenor should help the Treasury function in facilitating communication and coordination in relation to strategic priorities of the payments ecosystem, the review said.

The ministerial designation power, meanwhile, will allow the Treasurer to designate payment systems and participants of designated payment systems where it is in the national interest to do so. The designation power includes the power to direct regulators to develop regulatory rules and the power for the Treasurer to give binding directions to operators of, or participants in, payment systems

“Promoting a more innovative and robust payments environment is part of the Morrison government’s plan to build a more competitive and productive economy as we recover from the COVID-19 crisis,” Treasurer Josh Frydenberg said in a statement.

“The government will carefully consider the recommendations and observations made in the review. Consultation on the recommendations will be conducted by Treasury ahead of the government finalising a response before the end of the year.”